Model Portfolios

Building your retirement investment portfolio is a personal journey – there’s no one-size-fits-all. Your ideal portfolio is a reflection of your stage of life, your financial goals, and your comfort with risk. Most people begin investing for retirement by setting aside a percentage of their paycheck to contribute to their employer-sponsored retirement plan like a 401(k) or 403(b). These regular payroll deductions allow you to steadily accumulate mutual fund shares through Dollar Cost Averaging. The result is that more shares of each mutual fund are purchased when prices are relatively low and less are purchased when prices are relatively high. While target-date funds provide an easy hand-off approach in your 401(k), you may want more customization. The Traditional, Conservative, or Aggressive model portfolios offer examples to spark ideas – mix and match investments to suit your needs.

If you have been investing for your retirement you may actually have more than one investment portfolio. In addition to workplace accounts, you may hold IRAs, Roth IRAs, or personal brokerage investments. In these accounts you get to choose the asset classes, your asset allocation, and even get to select the individual Mutual Funds and ETFs to invest in. If you’ve made it past mid-career the Insightful Portfolio provides a more diversified asset allocations that includes alternatives to complement your stocks and bonds. If you’re knocking on the door of retirement the Retirement Portfolio takes this one step further by balancing the opportunity for growth with investment risks to keep you on tract for a fun-filled journey.

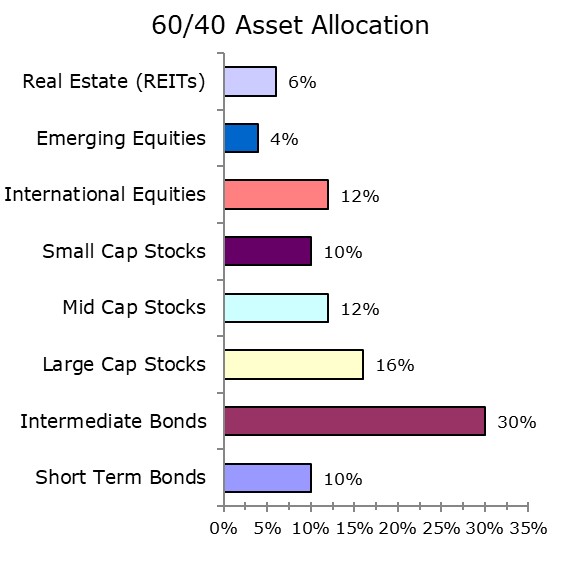

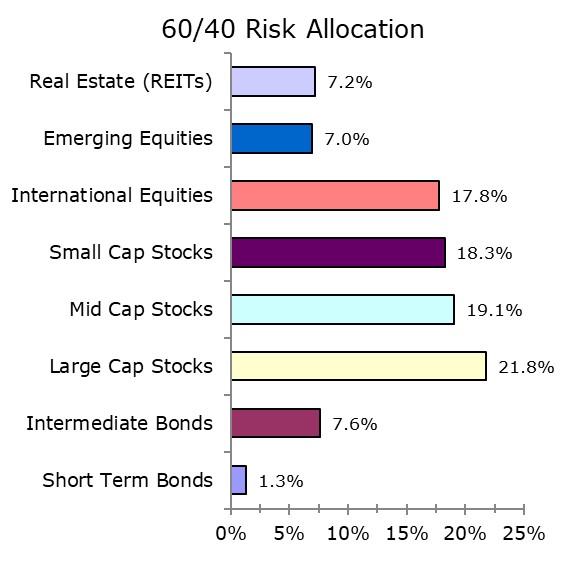

Traditional 60/40 Portfolio

The most talked about investment portfolio in the financial world is a moderate one that consists of 60% Stocks and 40% Bonds. While this traditional portfolio is considered pretty safe many would be surprised to learn that 90% of the risk in the portfolio comes from the 60% allocation to stocks. Don’t let that scare you. In order to have your investment grow over time you’ve got to take some investment risk. The best way to mitigate that risk is to have a long time horizon so this portfolio may suit you well if you have at least 10 years until retirement.

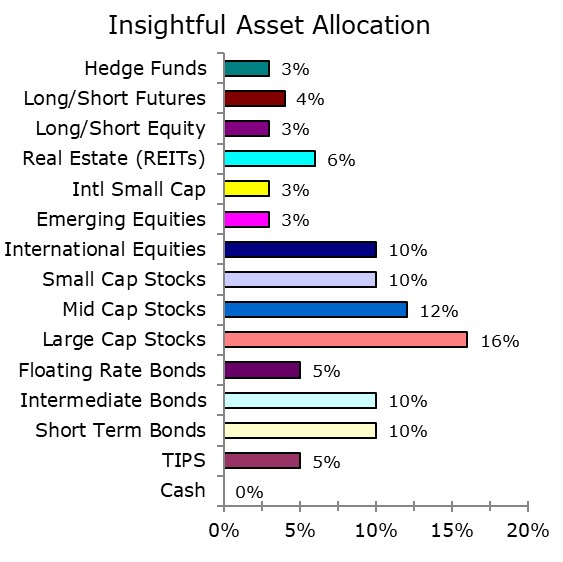

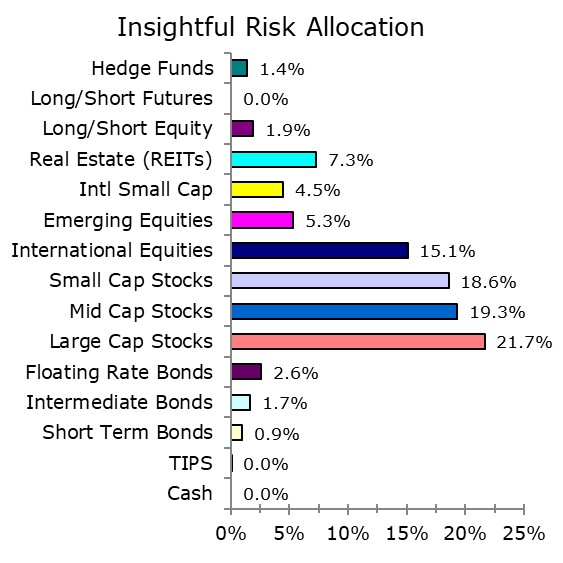

Insightful Asset Allocation

A better approach to asset allocation and portfolio diversification is to create a more diversified portfolio that has less exposure to equities and bonds than most people have. The Insightful Asset Allocation, has more asset classes than provided by target date funds or in most 401(k) plans. My choice would be to build a portfolio that takes takes 10% out of the Bond side of the Traditional 60% Stocks and 40% Bond portfolio and invest that 10% into hedged equities, long/short equity, and managed long/short futures. In addition, the bond portion of your portfolio should be more diversified than what is often available in employer sponsored plans.

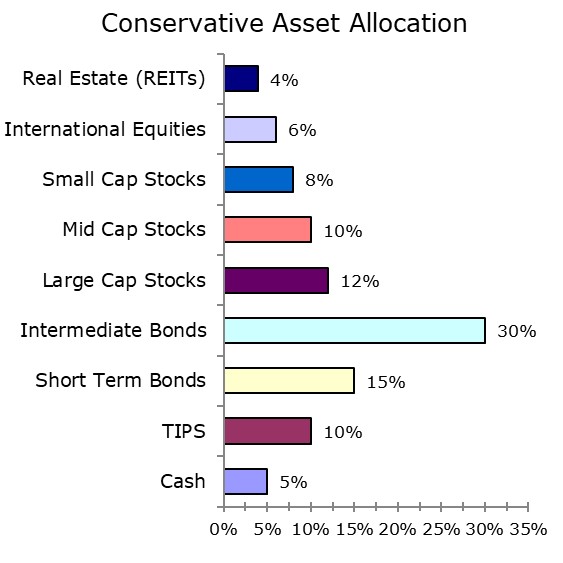

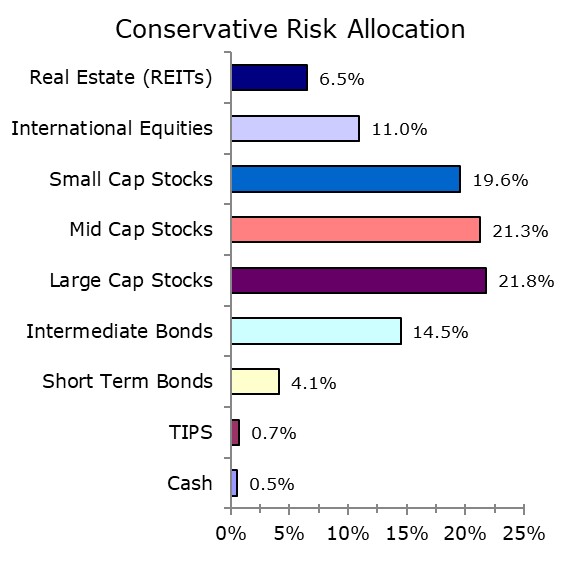

Conservative Asset Allocation

If you are getting close to retirement age, or you just have a very low tolerance for risk with your investments, you should reverse the traditional approach and reduce your exposure to equities to only about 40% while increasing your fixed income allocation to 60%. Even with this reduced allocation to equities, stocks will still make up the majority of risk in your investment portfolio. The Conservative Asset Allocation is as balanced of a risk profile as is practical, unless you look at the Retirement Asset Allocation.

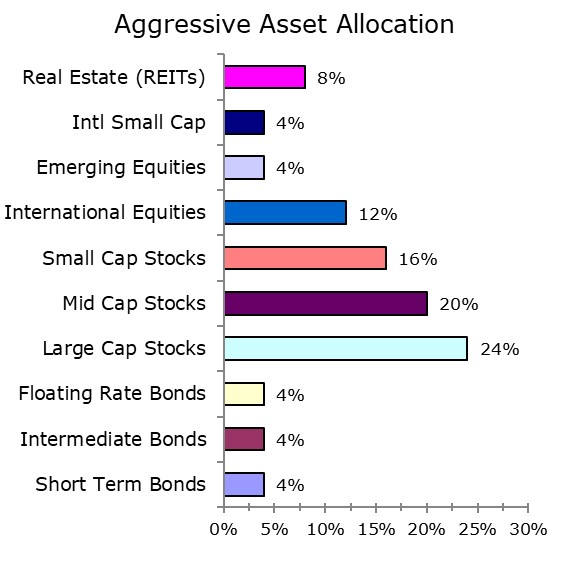

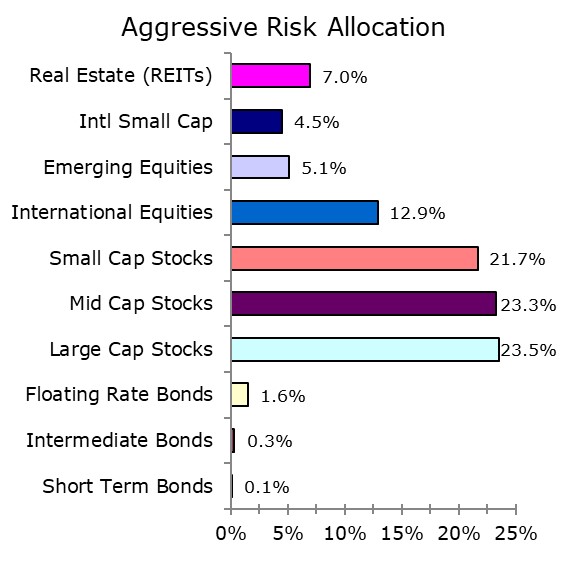

Aggressive Asset Allocation

While the Aggressive Asset Allocation portfolio won’t apply to most readers of this website, if you are young, have more than 25 years until retiring a significant allocation to stocks makes sense, but don’t go overboard. It helps to have a small allocation to bonds to rebalance your portfolio when stocks hit a down cycle.

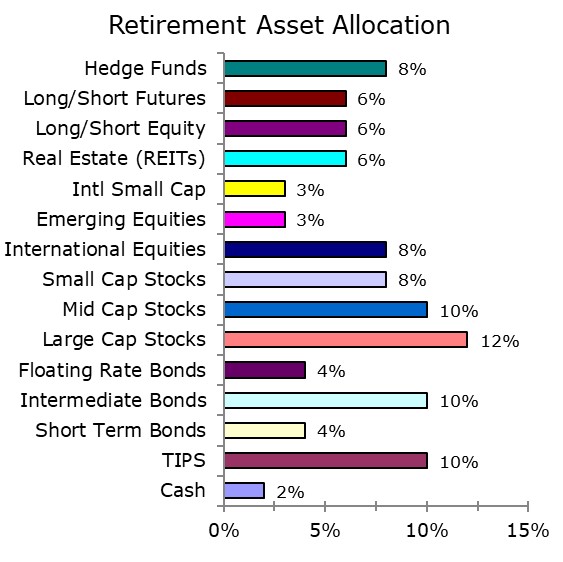

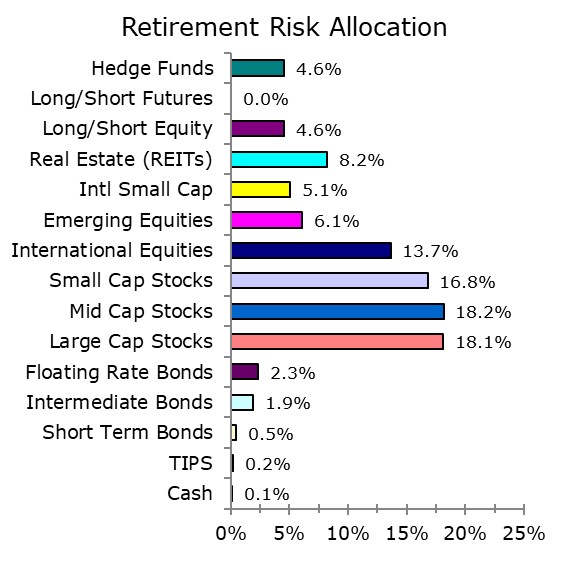

Retirement Asset Allocation

You do not want to throw all of your investments in cash when your retire, but then again you do not want to invest it all in the stock market. In retirement you should always have a couple of years of expenses available in cash and invest the rest in a diversified mix of stocks, bonds, and alternatives like the Retirement Asset Allocation portfolio. Balancing risk without limiting opportunities for growth is most important during retirement.