Mapping Your Journey to Retirement

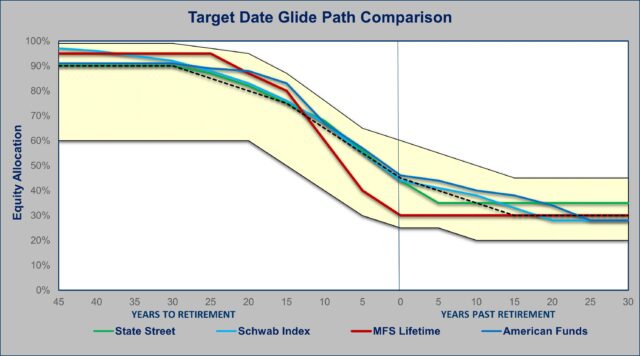

When it comes to target date funds, one of the biggest decisions you’ll make is choosing the right glide path. The glide path is like a roadmap that shows how your investment mix will shift over time as you approach and enter retirement. It determines how much risk you’ll take on and what kind of returns you might see, presenting a picture of how the fund’s equity exposure changes over your lifetime.

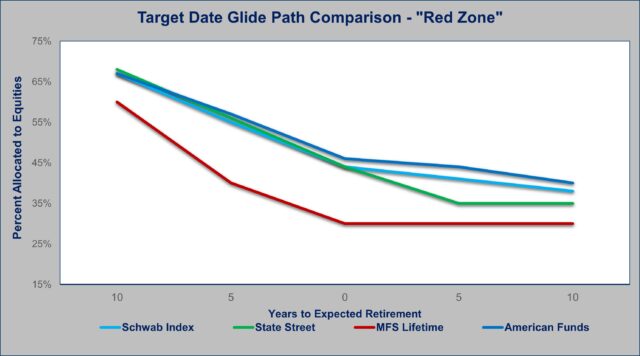

Understanding the difference between “To” and “Through” glide paths is key. The biggest distinctions come into play in what I call the “Retirement Red Zone” – the 10 years before and after your retirement date. I illustrate with some of my favorite Target Date fund series.

The “To” Glide Path: Winding Down for Retirement

Funds like the MFS Lifetime series us a “To” glide path. These are designed to shift your asset allocation to a more conservative investment mix by swiftly reducing stock exposure by the time you reach your target retirement date. This approach aims to preserve capital and mitigate risk as you near retirement. It’s similar to a football team strategically running down the clock in the final quarter to protect their lead. The landing point – when your mix locks in – coincides with your target retirement date.

Pros:

- Reduces risk in the ‘Retirement Red Zone’. This helps to protect your nest egg from potential market volatility and the potential of sequence of return risk.

- A more aggressive equity allocation in the early years of the accumulation phase has the potential for higher returns when your nest egg is focused on growth.

Cons:

- May limit returns in retirement due to a more conservative asset allocation at and after the target date.

- The conservative equity positioning may not provide sufficient long term growth after retirement to combat inflation and longevity risk during a long retirement.

The “Through” Glide Path: Prolonging the Journey

On the flip side, a “Through” glide path extends beyond the target retirement date, recognizing that retirement is just the beginning of a new chapter. That’s like a team continuing to play aggressively even after taking the lead. Most Target Date series, including the American Funds Target Date Retirement series, use this approach and have a landing point many years after retirement.

Pros:

- Provides continued risk management and growth potential during retirement.

- Higher equity allocations early in your retirement years can provide the growth necessary to combat inflation and longevity risk.

Cons:

- Potentially exposes your portfolio to higher equity risk in the ‘Retirement Red Zone” when preservation of capital may be a higher priority.

- An aggressive equity allocation exposes your portfolio to potential large losses in a bear market late in life that could severely impact the longevity of your investments.

A Few Words About Passive Index Approach to Glide Paths

If keeping costs low is a top priority, passive index target date funds like the Schwab Target Index series or the State Street Target Retirement series offer diversified market exposure at a lower cost than active funds. While passive strategies lack don’t adjust to market conditions, they do provide consistent market tracking and broad diversification, making them suitable for many investors. However, from my perspective, it’s important to remember the adage “you get what you pay for” – active management may deliver higher net returns over the long run.

Active vs. Passive Investment Management

The age-old debate between active and passive management rages on. In my experience there are some investments where active managers can add value, while in others passive index approaches make sense. The managers running active series like American Funds Target Date Retirement series or MFS Lifetime series can dynamically adjust allocations, potentially providing higher returns but at a higher cost. Passive index series like Schwab Target Index series or the State Street Target Retirement series offer diversified market exposure at a lower cost but without the potential benefits of active management. Target Date funds are one investment area where active managers often do add value.

Choosing Your Glide Path: A Balancing Act

The ideal Glide Path for you depends on your individual circumstances, risk tolerance and retirement goals. Here are some considerations to help guide your choice:

Choose a “To” Glide Path if:

- You are risk-averse and you want to prioritize capital preservation and stability nearing retirement.

- You have a clear idea of your retirement income needs and have other sources of income including Social Security, pensions, or annuities.

Choose a “Through” Glide Path if:

- You have a high risk tolerance, are comfortable with some market volatility, and expect a long retirement.

- You prioritize growth potential alongside income generation throughout retirement.

Choosing ‘Your’ Target Date

Most of you have access to a Target Date Fund in your 401(k) or 403(b) defined contribution retirement plan. While you may not be able to choose your Glide Path in your company plan, there are a couple of tweaks you can make the personalize your experience rather than accepting the default target date closest to the year you turn 65.

First, consider your actual planned retirement age. If you plan to retire earlier or later than 65, it may be wise to choose a fund with a target date that most closely aligns with your anticipated retirement timeline. If you plan to retire at 62 or earlier select the fund with a target date 5 years earlier. On the other hand if you plan to max out Social Security and retire at age 70, then choose a fund with a target date 5 years later.

Then evaluate your risk tolerance. In a similar way to your retirement date adjustment, if you are risk-averse and would prefer a more conservative glide path than the one available to you in your retirement plan, choose a fund with a target date that is 5 years earlier than your planned retirement date. On the other hand, if you feel the glide path of the fund on your retirement plan is not aggressive enough, choose a fund with a target date that is 5 years later than your planned retirement date.

Have you got all that? After considering these factors you may decide to choose the fund that has a Target Date that is 10 years before or 10 years after you would have been assigned based on the year you will turn 65. This approach ensures that the glide path is being used in a way that is suitable for you.

Glide Paths are a Journey, Not a Destination

At the end of the day, your glide path choice should align with your investment goals, risk tolerance, and retirement income needs. It’s essential to consider factors such as your desired lifestyle in retirement, potential longevity, and the role of other income sources like Social Security and pensions.

By understanding the intricacies of “To” and “Through” glide paths, as well as the potential landing points for “Through” glide paths, you can make an informed decision that aligns with your unique circumstances and investment objectives.

Remember, a Target Date Fund is a powerful tool, but it’s just one piece of your overall retirement plan.